The pivotal role of fixed income markets in the ESG revolution

Marketing communication

Pictet Asset Management & the Institute of International Finance (IIF)

Some might argue that building a sustainable economy is a technological problem. It isn’t. The world is sufficiently stocked with greenhouse gas-reducing technologies such as renewable fuels, carbon capture and energy storage. What it lacks is capital. According to the International Energy Agency, investments in clean energy alone will have to rise to an annual USD 4 trillion by the end of this decade to keep global warming in check. Realistically, funding on that scale can only come from the financial market. Bond investors in particular.

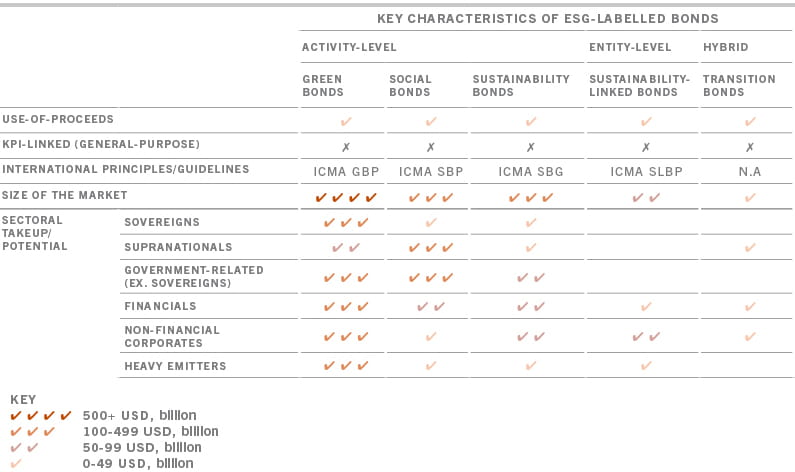

ESG bond characteristics

Source: IIF, as of December 2021

Encouragingly, fixed income markets appear to be up to the task. As governments, corporations and investors ramp up their climate commitments, securities that embed environmental, social and governance (ESG) considerations are in the ascendancy.

Green fixed income securities with specific use-of-proceeds requirements, sustainability-linked bonds with coupons tied to issuers’ environmental credentials and social bonds that fund educational programmes are just some examples of the innovative structures vying to go mainstream. Investors have responded enthusiastically so far. In 2021, over USD 1.1 trillion of new sustainable bonds were successfully placed, taking the size of the ESG bond market to well above USD 2 trillion. Research undertaken for Pictet by the Institute of International Finance suggests issuance could reach an annual pace of USD 4.5 trillion per year by 2025.

While most of that capital will be raised in the developed world, much of it can also be expected to come in the form of emerging market ESG bonds. It is essential that it does. For developing economies, private finance is crucial if they are to fulfil the UN Sustainable Development Goals (SDGs) by 2030.

Yet for sustainable debt to become mainstream, several obstacles need to be negotiated. The immediate priority is universal rules and standards. Currently, the labelling and certification of sustainable bonds differs considerably from one country to another, while efforts to harmonise disclosure requirements haven’t met with much success.

An analysis of the ESG securities with the longest track record – green bonds – reveals other potential trade-offs. Green bonds have delivered similar returns to non-green debt, yet they trade a premium: their yields tend to be persistently lower than those of traditional securities. This is despite the fact that green bonds are less liquid. Our analysis shows that such securities trade less often, in some cases far less often, than conventional fixed income. This reinforces our belief that purchasers of green and sustainability- linked bonds tend to be ‘buy and hold’ institutional investors such as pension funds, insurance funds and sovereign wealth funds. What it also suggests, however, is that the secondary market for such debt is not mature enough to absorb large buy or sell orders without precipitating significant shifts in price.

Ultimately, none of these hurdles are insurmountable. If world leaders are genuinely committed to net zero, they will also recognise that these ambitions require capital to flow freely. Which is why, in the battle against climate change, bond investors could soon find themselves in the front line.

Download paper

to discover how green bonds measure up as investments.

Authors

Sonja Gibbs , Managing Director & Head of Sustainable Finance at the Institute of International Finance (IIF) and, Raymond Sagayam Chief Investment Officer - Fixed Income at Pictet Asset Management